Cash out refinance allows you to get a lump sum for your mortgage balance. The loan agreement will be different than your original mortgage and will include a different interest rate, repayment term, and loan amount. This type of loan typically allows you to take out up to 30 years to repay the loan and can have a fixed or adjustable interest rate. The loan may be used for a variety of purposes, including home improvement or tax savings.

Refinance your mortgage with cash-out

If you want to pay off your existing mortgage and buy a new one, a cash-out refinance is a great option. These types are best for home renovations and have a lower downpayment. But, before you apply for one of these cash-out refinances, be sure to discuss the risks with a financial professional or accountant. Cash-out refinances will require that your property be appraised before you can obtain a cash advance.

Compared to other ways of leveraging home equity, cash-out refinances require only a single monthly payment. These refinances have a single monthly payment and can be used for anything, including debt consolidation and college tuition. The best thing about cash-out refinances are their lower interest rates. Cash-out refinances can be used to pay off high-interest credit card debts, saving you thousands in interest payments. Also, it can increase your credit score by paying off all of your credit card debts.

Home equity loans can be used as a second mortgage.

A home equity loan, a second mortgage that borrows against the homeowner's equity in their home, is a type which uses the home's equity as collateral. It is a great option to consolidate your debts into one low-interest payment and receive a lower rate of mortgage. These loans typically have fixed interest rates, monthly payments, and no surprises. Another benefit of home equity loans are that the funds are generally given in a lump sum so the borrower is able to budget accordingly.

The best part about home equity loans is that they are easy to obtain. They offer quick access to cash and are often tax-deductible. Although you will need to go through a credit check and order an appraisal of your home, the process is usually simple.

They are more expensive than cash-out refinances because they have higher interest rates

If you need large amounts of money quickly, a Cash-out Refinance is a viable option. It can cost more than a home equity loan, however. Cash-out refinances also require a good credit score and higher underwriting standards.

Refinance your mortgage with cash-out. In return, you'll only pay one monthly fee instead of many. Variable interest rates are available for home equity loans. These may increase over time. This means that you need to shop around for best rates and terms.

These allow you to withdraw money from your house before it is sold.

A home equity loan, or cash-out refinance, is a type if home loan that allows the borrower to take money out from their home before they sell it. The money can be used to pay off large debts or for other major expenses. Some borrowers use the money to fund education, emergency savings, or other large expenses. However, this type of loan comes with some disadvantages.

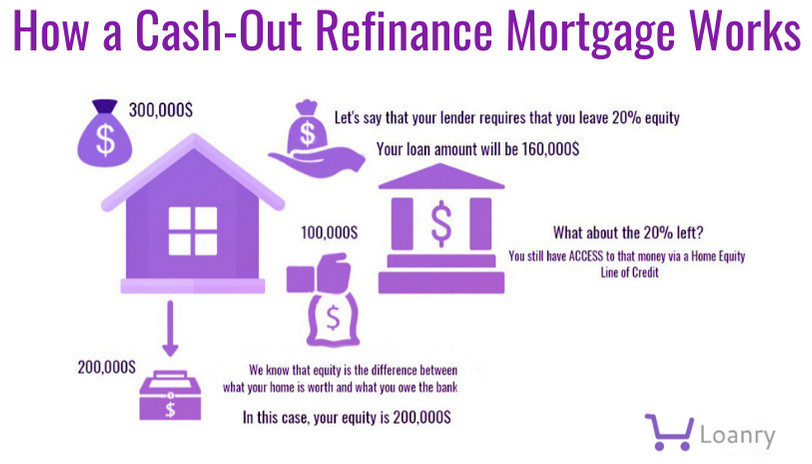

A cash-out refinance allows you to refinance your mortgage to a larger rate. You then receive a check at closing for the difference between the old and new mortgage balance. You can spend the money however you wish. According to a recent Freddie Mac study, the most popular use of a cash out refinance is to pay off debt. You can also use the cash to improve your home or go back to college.

FAQ

What should I look for in a mortgage broker?

Mortgage brokers help people who may not be eligible for traditional mortgages. They compare deals from different lenders in order to find the best deal for their clients. Some brokers charge a fee for this service. Others offer free services.

How can I get rid of termites & other pests?

Your home will be destroyed by termites and other pests over time. They can cause damage to wooden structures such as furniture and decks. It is important to have your home inspected by a professional pest control firm to prevent this.

What amount of money can I get for my house?

This can vary greatly depending on many factors like the condition of your house and how long it's been on the market. Zillow.com says that the average selling cost for a US house is $203,000 This

How long does it take to sell my home?

It depends on many factors, such as the state of your home, how many similar homes are being sold, how much demand there is for your particular area, local housing market conditions and more. It can take anywhere from 7 to 90 days, depending on the factors.

What are the downsides to a fixed-rate loan?

Fixed-rate loans are more expensive than adjustable-rate mortgages because they have higher initial costs. You may also lose a lot if your house is sold before the term ends.

What is a Reverse Mortgage?

Reverse mortgages allow you to borrow money without having to place any equity in your property. It works by allowing you to draw down funds from your home equity while still living there. There are two types to choose from: government-insured or conventional. With a conventional reverse mortgage, you must repay the amount borrowed plus an origination fee. FHA insurance covers the repayment.

What is the cost of replacing windows?

Replacement windows can cost anywhere from $1,500 to $3,000. The total cost of replacing all your windows is dependent on the type, size, and brand of windows that you choose.

Statistics

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

External Links

How To

How to manage a rental property

While renting your home can make you extra money, there are many things that you should think about before making the decision. We will show you how to manage a rental home, and what you should consider before you rent it.

Here's how to rent your home.

-

What is the first thing I should do? You need to assess your finances before renting out your home. If you have outstanding debts like credit card bills or mortgage payment, you may find it difficult to pay someone else to stay in your home while that you're gone. You should also check your budget - if you don't have enough money to cover your monthly expenses (rent, utilities, insurance, etc. It may not be worth it.

-

How much does it cost for me to rent my house? Many factors go into calculating the amount you could charge for letting your home. These factors include the location, size and condition of your home, as well as season. Prices vary depending on where you live so it's important that you don't expect the same rates everywhere. Rightmove estimates that the market average for renting a 1-bedroom flat in London costs around PS1,400 per monthly. If you were to rent your entire house, this would mean that you would earn approximately PS2,800 per year. It's not bad but if your property is only let out part-time, it could be significantly lower.

-

Is it worth it? It's always risky to try something new. But if it gives you extra income, why not? It is important to understand your rights and responsibilities before signing anything. Renting your home won't just mean spending more time away from your family; you'll also need to keep up with maintenance costs, pay for repairs and keep the place clean. Make sure you've thought through these issues carefully before signing up!

-

Are there any advantages? So now that you know how much it costs to rent out your home and you're confident that it's worth it, you'll need to think about the advantages. There are many reasons to rent your home. You can use it to pay off debt, buy a holiday, save for a rainy-day, or simply to have a break. Whatever you choose, it's likely to be better than working every day. Renting could be a full-time career if you plan properly.

-

How do I find tenants? Once you've made the decision that you want your property to be rented out, you must advertise it correctly. Online listing sites such as Rightmove, Zoopla, and Zoopla are good options. You will need to interview potential tenants once they contact you. This will enable you to evaluate their suitability and verify that they are financially stable enough for you to rent your home.

-

What are the best ways to ensure that I am protected? You should make sure your home is fully insured against theft, fire, and damage. You'll need to insure your home, which you can do either through your landlord or directly with an insurer. Your landlord will usually require you to add them as additional insured, which means they'll cover damages caused to your property when you're present. If your landlord is not registered with UK insurers, or you are living abroad, this policy doesn't apply. You will need to register with an International Insurer in this instance.

-

Even if your job is outside the home, you might feel you cannot afford to spend too much time looking for tenants. However, it is important that you advertise your property in the best way possible. Make sure you have a professional looking website. Also, make sure to post your ads online. Additionally, you'll need to fill out an application and provide references. While some people prefer to handle everything themselves, others hire agents who can take care of most of the legwork. In either case, be prepared to answer any questions that may arise during interviews.

-

What do I do when I find my tenant. If you have a lease in place, you'll need to inform your tenant of changes, such as moving dates. If you don't have a lease, you can negotiate length of stay, deposit, or other details. Keep in mind that you will still be responsible for paying utilities and other costs once your tenancy ends.

-

How do I collect my rent? When it comes time for you to collect your rent, check to see if the tenant has paid. You will need to remind your tenant of their obligations if they don't pay. Any outstanding rents can be deducted from future rents, before you send them a final bill. You can call the police if you are having trouble getting hold of your tenant. They will not usually evict someone unless they have a breached the contract. But, they can issue a warrant if necessary.

-

What can I do to avoid problems? While renting out your home can be lucrative, it's important to keep yourself safe. Consider installing security cameras and smoke alarms. Make sure your neighbors have given you permission to leave your property unlocked overnight and that you have enough insurance. Finally, you should never let strangers into your house, even if they say they're moving in next door.